What’s on the market in Lanikai: Homes with scintillating views

Lanikai is a highly sought-after destination for those who want to experience the good life. This little slice of paradise exemplifies Hawaii’s best qualities, and thus h...

Located on Oahu’s Windward Coast lies Kailua, a serene community surrounded by lush mountains and stunning beaches, friendly locals, and an appealing dining and retail scene that brings residents and visitors close to modern conveniences....

As is often said, timing is everything, and this is especially true when it comes to selling your home in Diamond Head O'ahu. If you’re planning to sell your home but aren’t sure about when and how, here’s our in-depth guide to Diamon...

The Beverly Hills of Oahu, HIi, Kahala is a beautiful neighborhood of luxury properties, turquoise beaches, palm-lined shores, and sunny weather all year round. And the best part? Kahala Beach is away from the crowd, perfect for those who...

In the midst of a global pandemic, our homes have become much more than a space that provides a roof over our heads. We've experienced sheltering in place for several months, so having a place we can call our own has become invaluable. For many...

You're almost there. You can’t wait to finally get your house keys and move to this new place you’d call home. You just can’t contain your excitement as the closing day approaches.

However, you’ve still got the final walkthrough—you...

Selecting and buying furniture for your beautiful abode, whether it be a sofa, dining table or any other piece, is no doubt fun and exciting. Especially if you're a first-time homeowner who finally has the liberty to choose whatever furniture y...

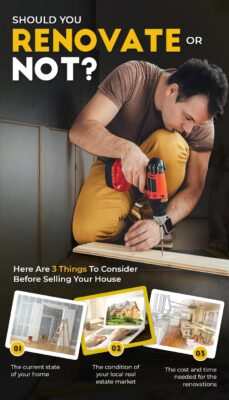

When thinking about putting their property on the market, homeowners often need to ponder on this question: should they renovate or not before selling? Since it's every home seller’s goal to make sure they get the best price for their biggest...

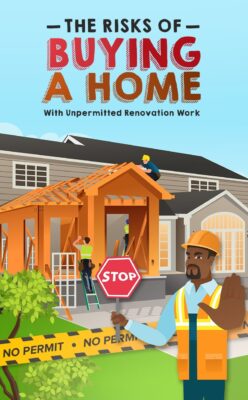

When you're on a search for your dream home, it’s easy enough to fall in love with any renovated features, such as a remodeled kitchen or bathroom, a finished basement, or a newly-installed deck, that are set to make your life more comfortabl...

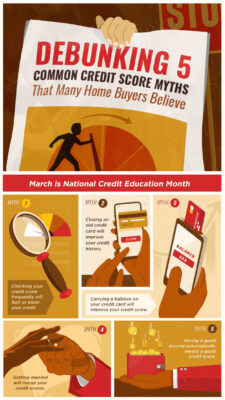

When it comes time to buy a home, a good credit score boosts your chances of getting a mortgage because it shows lenders or mortgage companies that you are likely to pay a loan on time. Thus, having a bad credit score can be a massive barrier t...